On the 5th March 2009, following some of the more turbulent times in our economic history, the BofE cut our base rate to 0.5% and announced that it was to start the process of pumping tens of billions of pounds of newly created money into Britain’s troubled economy. Whilst this day was significant for not just the actions of the BofE, it also started a frenzied search for income.

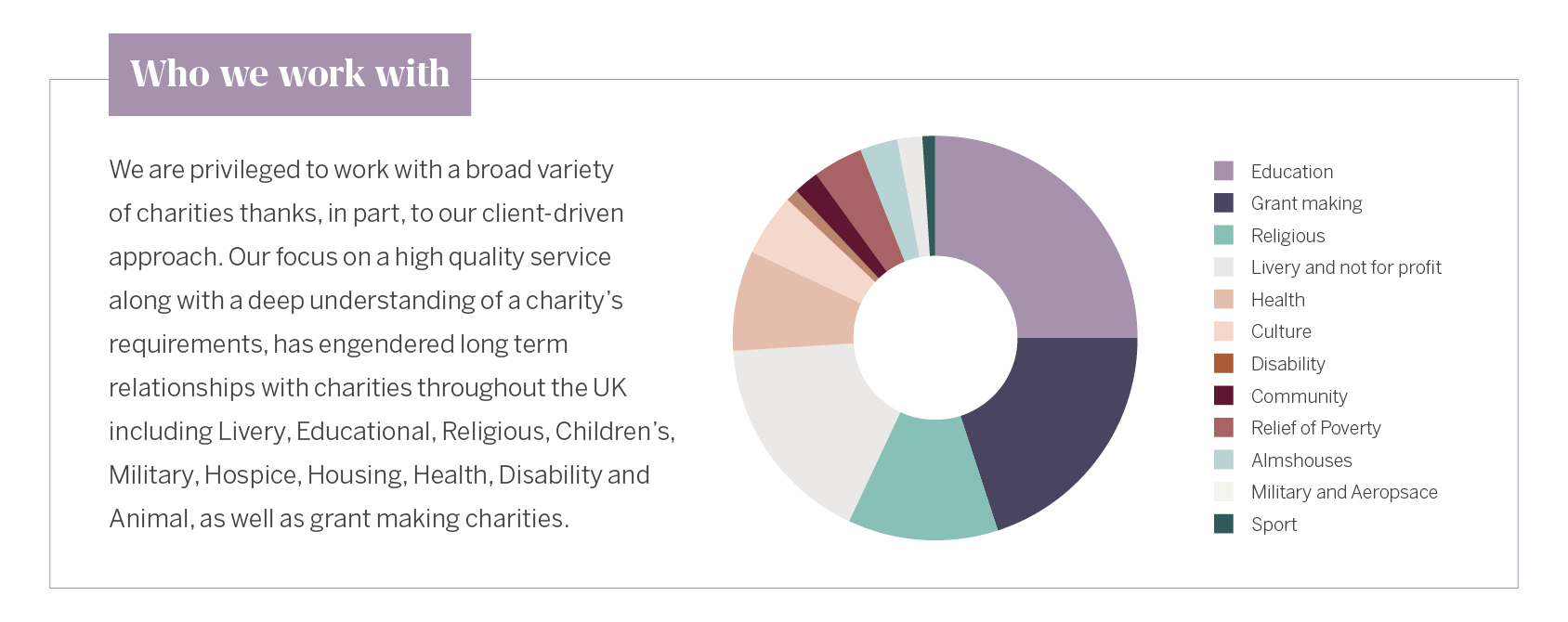

Raising funds has always been at the heart of charities’ activities but sometimes fundraising, in isolation, is not sufficient to meet objectives. Over the past 8 years, with the 10 year Gilt yield averaging close to 1% and returns on cash deposits negligible, generating income has been somewhat challenging. Dynamic asset allocation has been central to our approach as historically low bond allocations have had to be offset elsewhere in portfolios to generate this much needed income. Income levels have generally been maintained, albeit with a perceived increase in risk as equity allocations have increased and other asset classes have been introduced. Although we as a charities team have discussed these regularly over the last 10 years we thought it might be helpful to outline our current positioning and why we feel this perception of increased risk is somewhat misplaced.

Investments in certain infrastructure projects have been central to our approach in maintaining income levels for our charity clients. Given the long term nature of the underlying contracts with the public sector the dividends have been sustainable and remain so.

The dividends are fully covered by cashflows and the majority are index linked, providing inflation protection, whilst the asset class also has a low historic correlation to equities. Valuations of some infrastructure assets might appear stretched at present but with low yields on offer elsewhere and good asset management we continue to see its relative attractions.

Investments in certain infrastructure projects have been central to our approach in maintaining income levels for our charity clients.

Property has also played an integral role in generating an income whilst rising capital values have added a welcome boost to portfolios. When committing money to property we invest through closed ended structures which we feel is more suited to investing in an illiquid asset class. We have identified some excellent managers who, whilst they invest in different areas of the property market, they all have one thing in common in that highly desirable assets, whether they be industrial, office, residential or retail, remain central to their approach; this has served portfolios well. Yields have been squeezed but, like infrastructure assets, property continues to offer value when compared to cash and bonds.

We have discussed and debated at length with many trustees the need for Charities to allocate a higher proportion of capital to equities in order to help maintain income levels. This can be perfectly highlighted by the recent debt issue by Unilever who raised EUR350mn at 1.125% ( fixed rate) due in February 2022. With the equity yielding nearly 3x more and well covered, over the next 5 years the relative attractions are clear. Where we do hold fixed income, outside a few individual issues, we remain invested with highly experienced managers that adopt a more active approach. Whilst the income and capital returns have not been spectacular they continue to provide portfolios with a steady return and some uncorrelated exposure.

The key question is whether or not we need to change tack and we think not. Despite this recent interest rate increase, the bank rate remains near all-time lows and, although sterling made up a lot of ground just on talks of a rate rise, interestingly it fell immediately following the announcement suggesting the current outlook for monetary policy is more dovish than many anticipated. We certainly feel that our Charity portfolios are well positioned to meet their current and, maybe more importantly, future income expectations but the challenge to generate income certainly looks set to continue for a while longer.

Sam Barty-King, Senior Investment Manager and member of the charities team looks at the implications of the recent rate rise on charities and their trustees.